Wizards of the Coast regularly surveys various aspects of the adventure gaming channel; distributors, retailers and consumers to better understand their preferences, concerns, and needs. That data is regularly reviewed and distributed internally to senior management. The contents of this file are excerpts from those sources; the source materials themselves are confidential internal documents and are not available to the public.

Adventure Game Industry Market Research Summary (RPGs) V1.0

Release Date: February 07, 2000

Summary prepared by:

Ryan S. Dancey,

Vice President, Wizards of the Coast;

Brand Manager, Dungeons & Dragons

Permissions: This file is Copyright 2000, Wizards of the Coast. This file may be freely redistributed or quoted in whole or part, provided that this attribution remains intact.

Methodology: Wizards of the Coast regularly surveys various aspects of the adventure gaming channel; distributors, retailers and consumers to better understand their preferences, concerns, and needs. That data is regularly reviewed and distributed internally to senior management. The contents of this file are excerpts from those sources; the source materials themselves are confidential internal documents and are not available to the public. You have my assurances that to the best of my ability, the information presented in this document represents a fair and accurate representation of the data.

Sources: The primary source is a market segmentation study conducted in the summer of 1999. No confidential information provided by non-Wizards companies was used in the preparation of this report.

Exclusions: The internal information gathered by Wizards is considered an important competitive advantage. Therefore, not all the information available to Wizards is incorporated in this document, and there may be areas where substantial, significant information is purposefully not included. An effort has been made to ensure that the absence of any portion of this confidential information would not render the material provided herein inaccurate or invalid.

Pokemon Effect: As this study was conducted just as the Pokemon TCG phenomenon was gathering speed. For this, and several internal reasons, I have elected not to present information on the TCG component of the industry at this time.

Updates: From time to time, I intend to revise and update this file to reflect our ongoing efforts to understand the industry. When an update occurs, the version number of the document will be changed, as will the "release date". Interested parties can write to me at ryand@frpg.com to request an up to date copy of this document.

Section 1: The Segmentation Study

Since so much of this data is derived from the '99 Segmentation Study, it is important that the reader understand how this data was gathered.

For the purpose of the 1999 study, the following methodology was employed:

A two phase approach was used to determine information about trading card games (TCGs), role playing games (RPGs) and miniatures wargames (MWG) in the general US population between the ages of 12 and 35. For the rest of this document, this group is referred to as "the marketplace" or "the market", or "the consumers".

This age bracket was arbitrarily chosen on the basis of internal analysis regarding the probable target customers for the company's products. We know for certain that there are lots of gamers older than 35, especially for games like Dungeons & Dragons; however, we wanted to keep the study to a manageable size and profile. Perhaps in a few years a more detailed study will be done of the entire population.

Information from more than 65,000 people was gathered from a questionnaire sent to more than 20,000 households via a post card survey. This survey was used as a "screener" to create a general profile of the game playing population in the target age range, for the purposes of extrapolating trends to the general population.

This "screener" accurately represents the US population as a whole; it is a snapshot of the entire nation and is used to extrapolate trends from more focused surveys to the larger market.

A follow up survey was completed by about a thousand respondents from the "screener". The follow up survey is an extensive document with more than 100 questions. The particular individuals chosen to participate in this expanded survey represent the population, as determined by the screener. In other words, the small detailed survey group can be reasonably extrapolated to the larger screener group, and the larger screener group can be logically extrapolated to the public in general. This is a common, standard, and accepted methodology within the market research field.

The data from the detailed survey was collated and prepared by the Wizards market Research Department, in conjunction with an external consulting firm. We believe that the data is a fair and accurate representation of the hobby game consumer profile and that it does statistically correlate with the population as a whole in the US for the target age bracket.

Section 2: Basic Terms

As a part of the detailed survey, the following terms and examples were provided to the respondents:

Specific questions were also designed to separate users of "computer Role Playing Games" vs. "paper Role Playing Games".

(*) For my own purposes, I choose to use the term "Tabletop RPGs" in this document; the term "paper RPGs" was used in the study. The terms are synonyms; my choice is simply personal. I believe that in the fairly near future "paper" RPGs will hybridize with computer assistance ñ not becoming "computer RPGs" as that term is commonly understood, but not being games played simply with paper anymore either. Consider this a "forward looking" terminology.

The term "D&D" is used herein to describe all flavors and types of D&D play; from old "white box" players up to people playtesting 3rd Edition.

Section 3: Basic Demographics

The study provides the following information about the basic demographics of the tabletop RPG marketplace:

Tabletop RPGs

The study provides the following information about the basic demographics of the computer RPG marketplace:

Computer RPGs

The study provides the following information about the basic demographics of the MWG marketplace:

Miniatures/War Games

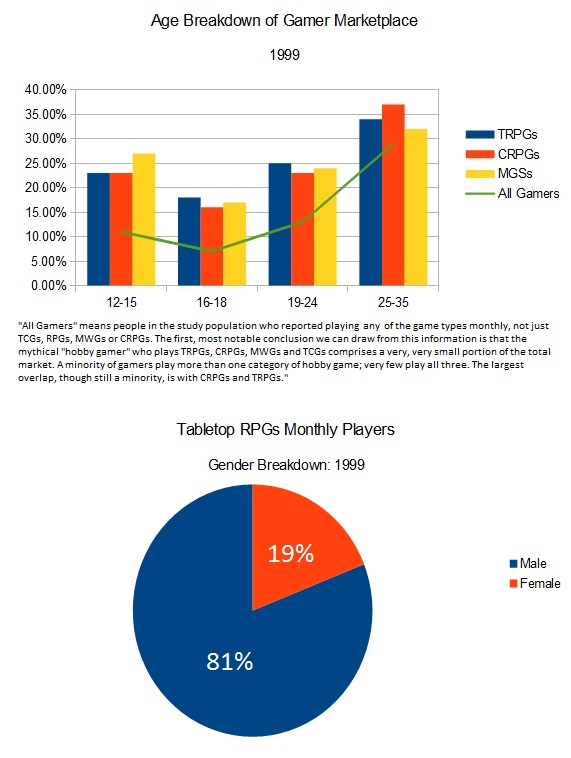

The age breakdown of players within the marketplace is:

(*) "All Gamers" means people in the study population who reported playing >any< of the game types monthly, not just TCGs, RPGs, MWGs or CRPGs.

Conclusions:

1. Few "General Gamers":

The first, most notable conclusion we can draw from this information is that the mythical "hobby gamer" who plays TRPGs, CRPGs, MWGs and TCGs comprises a very, very small portion of the total market. A minority of gamers play more than one category of hobby game; very few play all three. The largest overlap, though still a minority, is with CRPGs and TRPGs.

This is an exciting conclusion, because it indicates that a company can successfully create brand in one of the three hobby categories, and extend that brand into the other two without significantly cannibalizing sales. In other words, the people who buy the RPG are not likely to be the ones buying the MWG or the TCG.

2. There are "Women in Gaming"

Second, it is clear that female gamers constitute a significant portion of the hobby gaming audience; essentially a fifth of the total market. This represents a total population of several million active female hobby gamers. However, females, as a group, spend less than males on the hobby.

3. Adventure Gaming is an adult hobby

More than half the market for hobby games is older than 19. There is a substantial "dip" in incidence of play from 16-18. This lends credence to the theory that most people are introduced to hobby gaming before high-school and play quite a bit, then leave the hobby until they reach college, and during college they return to the hobby in significant numbers.

It may also indicate that the existing group of players is aging and not being refreshed by younger players at the same rate as in previous years.

Section 4: The Role of Computers

There is an intense, ongoing discussion between publishers and customers about the use of computers and the interaction between computer game play and adventure game play. The market research study presented some revealing insights into this ongoing debate.

Internet Gaming: 51% of the TRPG players report that they have ever played a game on the internet. 28% report that they play an internet game monthly.

% Who want to buy software to help manage game and speed up combat: 52%

% Who want to play D&D over the internet with others: 50%

% Who read newsgroups, mailing lists and web sites: 37%

% Who currently play with computer assistance: 42%

What computer do gamers use?

Wintel Platform: 63%

Macintosh Platform: 9%

(The question was essentially "What platform have you used in the last month", and "none" was an option, probably accounting for the missing percentage.)

What's sitting at home?

Wintel Platform: 54%

Macintosh Platform: 7%

Three quarters of the sample use the Internet at least once a week, but only two thirds have access from home.

"Who plays electronic games?"

Games electronic gamers play monthly

One conclusion we draw from this data is that people who play electronic games still find time to play TRPGs; it appears that these two pursuits are "complementary" or "noncompetitive" outside the scope of the macroeconomic "disposable income" competition.

Section 5: Tabletop RPG Business

We asked questions of people who play TRPGs to get a better and more detailed picture of that category. This section explores some of that data.

The market research study provides some useful information on the games TRPG players play when they're not role playing:

51% play a non-TCG card game monthly

43% play a puzzle computer game monthly

43% play a classic board game monthly

58% play an "action/shooter" computer game monthly

41% play a "simulation" computer game monthly

The >least< played game types were:

26% play a TCG monthly

24% play a puzzle table game monthly

17% play a MWG monthly

17% play a social/party game monthly

When asked how likely a person was to be the DM/GM, the responses were:

2+ Sessions as DM/GM: 47%

Don't DM/GM: 41%

When asked to describe a variety of past game experiences, the market provided the following data:

(*) Looked at in reverse, this interesting answer tells us that 14% of the gamers who play an RPG >have never played< a combat oriented RPG.

Of the people who reported playing a TRPG, we further screened for people who played D&D and asked those individuals some more detailed questions. This data comes from people who have played D&D, not necessarily those who play monthly.

One conclusion we drew from the data was that if a player had played longer than one year, the chances they would play another year were greater than if they had not yet been playing for a full year. In fact, the longer a person plays, the higher the chance they will stay in the game; in other words, players are >less< likely to quit playing D&D the longer they play, not >more< likely.

We asked what the frequency of play was:

(This data actually reads 7.2 4.9 13.2 5.9; I'm not sure what the extra column is - Morrus)

So we see that the longer a player is in the game, the fewer times per month they play after the 5th year. Once the "acquisition" period (1st year) has passed, frequency of play accelerates tremendously, then drops. One explanation for this fact may be that since acquisition happens most often at age 15 or less, "new players" may have a lot of time available for gaming, but as they age, they have less time per month to play.

We looked at a few other questions based on how long a person had been playing the game:

[ if this chart gets mangled in the formatting, it has three columns of data ]

(*) Remember that frequency of play is down sharply for these gamers)

This data tells us that the longer a person plays the game, the longer the game sessions get, the more people play in the game, and the longer the game progresses before a character restart. In fact, if you look at the >5 year group, you realize that the big jump in long sessions and in average sessions before a restart means that the 5+ year gamers are playing the same characters, on average, vastly longer than anyone else.

One conclusion might be that it takes 5 years for a player to really master the system and really figure out what kind of character that player likes to play.

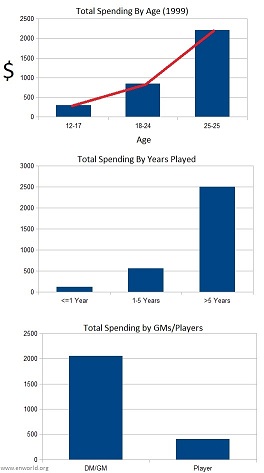

The following financial figures are for TRPG players in general (D&D information, where available, is provided as well)

This data seems to validate the theory that young gamers, while very active, don't spend a lot of money. (The following data is reported by for RPG expenditures) The big dollars come from adults...

Total spending by age:

12-17: $297

18-24: $850

25-25: $2,213

And, the longer they stay in the category, the greater their total outlays...

Play <=1 Year: $116

Play 1-5 Years: $562

Play >5 Years: $2,502

And if they can be induced to become a DM/GM, expenditures skyrocket.

Will DM/GM: $2,048

Will not DM/GM: $401

Some breakouts for the D&D population in particularÖ

Total D&D spending by age:

12-17: $164

18-24: $443

25-35: $1,642

Monthly D&D spending by age:

12-17: $10

18-24: $12

25-35: $14

Total D&D spending by time in game:

<=1 Year: $123

1-5 Years: $338

Monthly D&D spending by time in game:

<=1 Year: $7

1-5 Years: $22

5 Years: $16

(Interesting note: Monthly spending in the first five years after adoption of the game is higher than the spending beyond that point ñ though the older, longer gamer plays the game more, they spend less. This may relate to the frequency of a character/game restart.)

D&D DM willingness effect on expenditures:

Will DM: $1,444 total / $21 monthly

Will not DM: $187 total / $7 monthly

(Interesting note here: Even people who don't DM buy a heck of a lot more than just a PHB...)

Effect of miniatures addition to RPG mix:

Few miniatures owned/used: $139 total RPG spending

Many minis owned/used: $4,413 total RPG spending

We found that players who were ëlapsed' ñ reported that they had played TRPGs but were not currently doing so; had spent more money than the current players, and had played more different games monthly ñ but interestingly, they had spent less money, on average, on D&D than players who were "current".

Current/Lapsed

One conclusion that could be drawn from this data is that gamers who don't like D&D will spend a lot of money and try a lot of systems to find something they do like before they quit. Gamers who like D&D will spend less money and try fewer systems, but will spend more on D&D than those who don't.

When asked why a gamer lapsed, the answers (multiple choices allowed) were:

Got too busy with other things: 79%

Too few people to play with: 63%

Not enough time to play: 55%

Found a game I liked better: 38%

Unhappy with the game and the rules: 38%

Cost too much money: 32%

Burnt out from frequent play: 29%

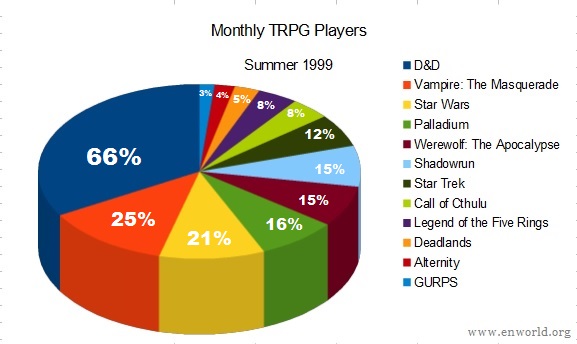

Getting back to the people still playing the games, when asked what games TRPG players play monthly, the answers (multiple choices allowed) were:

D&D: 66%

Vampire: The Masquerade: 25%

Star Wars: 21%

Palladium: 16%

Werewolf: The Apocalypse: 15%

Shadowrun: 15%

Star Trek: 12%

Call of Cthulu: 8%

Legend of the Five Rings: 8%

Deadlands: 5%

Alternity: 4%

GURPS: 3%

When asked to describe aspects of their games, on a scale from 1 to 5, answers were:

When we asked RPG purchasers how many had purchased D&D at a particular retail type, the answers were:

(*)Hobby/game shops: 36%

Book Stores: 27%

Comic book stores: 18%

Specialty toy and game: 17%

Large toy store chains: 15%

Conventions: 4%

(In other words, 36% of the respondents indicated they had purchased a D&D product at a Hobby/Game shop.)

Adventure Game Industry Market Research Summary (RPGs) V1.0

Release Date: February 07, 2000

Summary prepared by:

Ryan S. Dancey,

Vice President, Wizards of the Coast;

Brand Manager, Dungeons & Dragons

Permissions: This file is Copyright 2000, Wizards of the Coast. This file may be freely redistributed or quoted in whole or part, provided that this attribution remains intact.

Methodology: Wizards of the Coast regularly surveys various aspects of the adventure gaming channel; distributors, retailers and consumers to better understand their preferences, concerns, and needs. That data is regularly reviewed and distributed internally to senior management. The contents of this file are excerpts from those sources; the source materials themselves are confidential internal documents and are not available to the public. You have my assurances that to the best of my ability, the information presented in this document represents a fair and accurate representation of the data.

Sources: The primary source is a market segmentation study conducted in the summer of 1999. No confidential information provided by non-Wizards companies was used in the preparation of this report.

Exclusions: The internal information gathered by Wizards is considered an important competitive advantage. Therefore, not all the information available to Wizards is incorporated in this document, and there may be areas where substantial, significant information is purposefully not included. An effort has been made to ensure that the absence of any portion of this confidential information would not render the material provided herein inaccurate or invalid.

Pokemon Effect: As this study was conducted just as the Pokemon TCG phenomenon was gathering speed. For this, and several internal reasons, I have elected not to present information on the TCG component of the industry at this time.

Updates: From time to time, I intend to revise and update this file to reflect our ongoing efforts to understand the industry. When an update occurs, the version number of the document will be changed, as will the "release date". Interested parties can write to me at ryand@frpg.com to request an up to date copy of this document.

Section 1: The Segmentation Study

Since so much of this data is derived from the '99 Segmentation Study, it is important that the reader understand how this data was gathered.

For the purpose of the 1999 study, the following methodology was employed:

A two phase approach was used to determine information about trading card games (TCGs), role playing games (RPGs) and miniatures wargames (MWG) in the general US population between the ages of 12 and 35. For the rest of this document, this group is referred to as "the marketplace" or "the market", or "the consumers".

This age bracket was arbitrarily chosen on the basis of internal analysis regarding the probable target customers for the company's products. We know for certain that there are lots of gamers older than 35, especially for games like Dungeons & Dragons; however, we wanted to keep the study to a manageable size and profile. Perhaps in a few years a more detailed study will be done of the entire population.

Information from more than 65,000 people was gathered from a questionnaire sent to more than 20,000 households via a post card survey. This survey was used as a "screener" to create a general profile of the game playing population in the target age range, for the purposes of extrapolating trends to the general population.

This "screener" accurately represents the US population as a whole; it is a snapshot of the entire nation and is used to extrapolate trends from more focused surveys to the larger market.

A follow up survey was completed by about a thousand respondents from the "screener". The follow up survey is an extensive document with more than 100 questions. The particular individuals chosen to participate in this expanded survey represent the population, as determined by the screener. In other words, the small detailed survey group can be reasonably extrapolated to the larger screener group, and the larger screener group can be logically extrapolated to the public in general. This is a common, standard, and accepted methodology within the market research field.

The data from the detailed survey was collated and prepared by the Wizards market Research Department, in conjunction with an external consulting firm. We believe that the data is a fair and accurate representation of the hobby game consumer profile and that it does statistically correlate with the population as a whole in the US for the target age bracket.

Section 2: Basic Terms

As a part of the detailed survey, the following terms and examples were provided to the respondents:

| Term | Example |

| Paper RPGs* | Dungeons & Dragons |

| Card Games | Bridge, Solitaire, Uno, Poker |

| Trading Card Games | Magic, Pokemon |

| Word/ knowledge | Scrabble, Trivial Pursuit |

| Puzzle computer games | Tetris |

| Non-competitive problem solving | Sim City, Myst |

| Puzzle table games | Jenga, Dominoes |

| Class board games | Chess, Monopoly, Go |

| Action/Shooter/Arcade | Doom, Mortal Kombat |

| Miniatures table-top fantasy/sci-fi | Warhammer |

| Games that use miniatures | Battletech |

| War games | Historical Simulations |

| Simulations | Flight/car Simulators |

| Strategy games | Risk, Civilization |

| Social/party games | Charades, Pictionary |

| Strategic sport simulations | Madden, MLB |

| Other non-sport games | N/A |

(*) For my own purposes, I choose to use the term "Tabletop RPGs" in this document; the term "paper RPGs" was used in the study. The terms are synonyms; my choice is simply personal. I believe that in the fairly near future "paper" RPGs will hybridize with computer assistance ñ not becoming "computer RPGs" as that term is commonly understood, but not being games played simply with paper anymore either. Consider this a "forward looking" terminology.

The term "D&D" is used herein to describe all flavors and types of D&D play; from old "white box" players up to people playtesting 3rd Edition.

Section 3: Basic Demographics

The study provides the following information about the basic demographics of the tabletop RPG marketplace:

Tabletop RPGs

| Size 6% play or have played TRPGs (~ 5.5 million people) 3% play monthly (~ 2.25 million people) Gender 19% are female (monthly players) Crossover 17% of the total play MWGs monthly 46% of the total play computer RPGs monthly 26% of the total play TCGs monthly |

Computer RPGs

| Size: 8% play or have played CRPGs (~7.3 million people) 5% play monthly (~4.5 million people) Gender 21% are female Crossover 33% of the total play tabletop RPGs monthly 21% of the total play TCGs monthly 13% of the total play MWGs monthly |

Miniatures/War Games

| Size 4% play or have played MWGs (~3.7 million people) 2% play monthly (~1.8 million people) Gender 21% are female Crossover 37% play tabletop RPGs 40% play computer RPGs 29% play TCGs |

| Age | TRPG | MWG | CRPG | All Gamers(*) |

| 12-15 | 23% | 27% | 23% | 11% |

| 16-18 | 18% | 17% | 16% | 7% |

| 19-24 | 25% | 24% | 23% | 13% |

| 25-35 | 34% | 32% | 37% | 29% |

Conclusions:

1. Few "General Gamers":

The first, most notable conclusion we can draw from this information is that the mythical "hobby gamer" who plays TRPGs, CRPGs, MWGs and TCGs comprises a very, very small portion of the total market. A minority of gamers play more than one category of hobby game; very few play all three. The largest overlap, though still a minority, is with CRPGs and TRPGs.

This is an exciting conclusion, because it indicates that a company can successfully create brand in one of the three hobby categories, and extend that brand into the other two without significantly cannibalizing sales. In other words, the people who buy the RPG are not likely to be the ones buying the MWG or the TCG.

2. There are "Women in Gaming"

Second, it is clear that female gamers constitute a significant portion of the hobby gaming audience; essentially a fifth of the total market. This represents a total population of several million active female hobby gamers. However, females, as a group, spend less than males on the hobby.

3. Adventure Gaming is an adult hobby

More than half the market for hobby games is older than 19. There is a substantial "dip" in incidence of play from 16-18. This lends credence to the theory that most people are introduced to hobby gaming before high-school and play quite a bit, then leave the hobby until they reach college, and during college they return to the hobby in significant numbers.

It may also indicate that the existing group of players is aging and not being refreshed by younger players at the same rate as in previous years.

Section 4: The Role of Computers

There is an intense, ongoing discussion between publishers and customers about the use of computers and the interaction between computer game play and adventure game play. The market research study presented some revealing insights into this ongoing debate.

Internet Gaming: 51% of the TRPG players report that they have ever played a game on the internet. 28% report that they play an internet game monthly.

% Who want to buy software to help manage game and speed up combat: 52%

% Who want to play D&D over the internet with others: 50%

% Who read newsgroups, mailing lists and web sites: 37%

% Who currently play with computer assistance: 42%

What computer do gamers use?

Wintel Platform: 63%

Macintosh Platform: 9%

(The question was essentially "What platform have you used in the last month", and "none" was an option, probably accounting for the missing percentage.)

What's sitting at home?

Wintel Platform: 54%

Macintosh Platform: 7%

Three quarters of the sample use the Internet at least once a week, but only two thirds have access from home.

"Who plays electronic games?"

| Computer | Console/Handheld | Both | |

| Average Age | 26 | 23 | 20 |

| Education | |||

| % 6th-8th | 5% | 20% | 27% |

| % 9th-12th | 23% | 52% | 37% |

| % College | 53% | 26% | 31% |

| % Post Grad | 20% | 2% | 5% |

| Marital Status | |||

| % Single | 52% | 65% | 76% |

| % Partnered | 46% | 29% | 22% |

Games electronic gamers play monthly

| Computer | Console/Handheld | Both | |

| TRPGs | 72% | 54% | 57% |

| CRPGs | 44% | 21% | 50% |

| Puzzle Comp | 39% | 41% | 49% |

| Classic Board | 39% | 48% | 44% |

| Action/Shooter | 32% | 55% | 61% |

| Simulations | 25% | 36% | 40% |

| Strategy Games | 26% | 26% | 32% |

Section 5: Tabletop RPG Business

We asked questions of people who play TRPGs to get a better and more detailed picture of that category. This section explores some of that data.

The market research study provides some useful information on the games TRPG players play when they're not role playing:

51% play a non-TCG card game monthly

43% play a puzzle computer game monthly

43% play a classic board game monthly

58% play an "action/shooter" computer game monthly

41% play a "simulation" computer game monthly

The >least< played game types were:

26% play a TCG monthly

24% play a puzzle table game monthly

17% play a MWG monthly

17% play a social/party game monthly

When asked how likely a person was to be the DM/GM, the responses were:

2+ Sessions as DM/GM: 47%

Don't DM/GM: 41%

When asked to describe a variety of past game experiences, the market provided the following data:

| Question | Result |

| Used detailed tables & charts | 76% |

| Included Miniatures | 56% |

| Used "rules light" system | 58% |

| Diceless | 33% |

| Combat Oriented | 86%* |

| Live Action | 49% |

| House Rules | 80% |

Of the people who reported playing a TRPG, we further screened for people who played D&D and asked those individuals some more detailed questions. This data comes from people who have played D&D, not necessarily those who play monthly.

| Age | <12 | 12-15 | 16-18 | 19-24 | 25-35 |

| Learned D&D | 23% | 41% | 15% | 12% | 9% |

| <= 1 Year | 1-5 Years | > 5 Years | |

| Expect another Year | 40% | 75% | 88% |

| Total D&D | <= 1 Year | 1-5 Years | >5 Years |

| Monthly | 7.2 | 13.2 | 5.9 |

So we see that the longer a player is in the game, the fewer times per month they play after the 5th year. Once the "acquisition" period (1st year) has passed, frequency of play accelerates tremendously, then drops. One explanation for this fact may be that since acquisition happens most often at age 15 or less, "new players" may have a lot of time available for gaming, but as they age, they have less time per month to play.

We looked at a few other questions based on how long a person had been playing the game:

[ if this chart gets mangled in the formatting, it has three columns of data ]

| Typical 4 or More Average Sessions | Session Gamers In before Restart | 5+ Hours Group (New Characters) | |

| Total | 28% | 62% | 15.4 |

| <=1 Year | 10% | 48% | 8.8 |

| 1-5 Years | 14% | 60% | 12.9 |

| >5 Years* | 42% | 71% | 19.6 |

This data tells us that the longer a person plays the game, the longer the game sessions get, the more people play in the game, and the longer the game progresses before a character restart. In fact, if you look at the >5 year group, you realize that the big jump in long sessions and in average sessions before a restart means that the 5+ year gamers are playing the same characters, on average, vastly longer than anyone else.

One conclusion might be that it takes 5 years for a player to really master the system and really figure out what kind of character that player likes to play.

The following financial figures are for TRPG players in general (D&D information, where available, is provided as well)

This data seems to validate the theory that young gamers, while very active, don't spend a lot of money. (The following data is reported by for RPG expenditures) The big dollars come from adults...

Total spending by age:

12-17: $297

18-24: $850

25-25: $2,213

And, the longer they stay in the category, the greater their total outlays...

Play <=1 Year: $116

Play 1-5 Years: $562

Play >5 Years: $2,502

And if they can be induced to become a DM/GM, expenditures skyrocket.

Will DM/GM: $2,048

Will not DM/GM: $401

Some breakouts for the D&D population in particularÖ

Total D&D spending by age:

12-17: $164

18-24: $443

25-35: $1,642

Monthly D&D spending by age:

12-17: $10

18-24: $12

25-35: $14

Total D&D spending by time in game:

<=1 Year: $123

1-5 Years: $338

5 Years: 1,756

Monthly D&D spending by time in game:

<=1 Year: $7

1-5 Years: $22

5 Years: $16

(Interesting note: Monthly spending in the first five years after adoption of the game is higher than the spending beyond that point ñ though the older, longer gamer plays the game more, they spend less. This may relate to the frequency of a character/game restart.)

D&D DM willingness effect on expenditures:

Will DM: $1,444 total / $21 monthly

Will not DM: $187 total / $7 monthly

(Interesting note here: Even people who don't DM buy a heck of a lot more than just a PHB...)

Effect of miniatures addition to RPG mix:

Few miniatures owned/used: $139 total RPG spending

Many minis owned/used: $4,413 total RPG spending

We found that players who were ëlapsed' ñ reported that they had played TRPGs but were not currently doing so; had spent more money than the current players, and had played more different games monthly ñ but interestingly, they had spent less money, on average, on D&D than players who were "current".

Current/Lapsed

| Mean RPG Spending | Mean D&D Spending | Total RPGs Played |

| $1,273 / $1,667 | $895 / $599 | 2.2 / 3.3 |

When asked why a gamer lapsed, the answers (multiple choices allowed) were:

Got too busy with other things: 79%

Too few people to play with: 63%

Not enough time to play: 55%

Found a game I liked better: 38%

Unhappy with the game and the rules: 38%

Cost too much money: 32%

Burnt out from frequent play: 29%

Getting back to the people still playing the games, when asked what games TRPG players play monthly, the answers (multiple choices allowed) were:

D&D: 66%

Vampire: The Masquerade: 25%

Star Wars: 21%

Palladium: 16%

Werewolf: The Apocalypse: 15%

Shadowrun: 15%

Star Trek: 12%

Call of Cthulu: 8%

Legend of the Five Rings: 8%

Deadlands: 5%

Alternity: 4%

GURPS: 3%

When asked to describe aspects of their games, on a scale from 1 to 5, answers were:

| Normally | Rarely | |

| Create Own Adventures | 42% | 11% |

| Create Own Campaign Material | 29% | 17% |

| Replay Adventures | 18% | 35% |

| Use adventures from magazines | 21% | 40% |

| Follow official D&D Rules | 33% | 17% |

(*)Hobby/game shops: 36%

Book Stores: 27%

Comic book stores: 18%

Specialty toy and game: 17%

Large toy store chains: 15%

Conventions: 4%

(In other words, 36% of the respondents indicated they had purchased a D&D product at a Hobby/Game shop.)

")